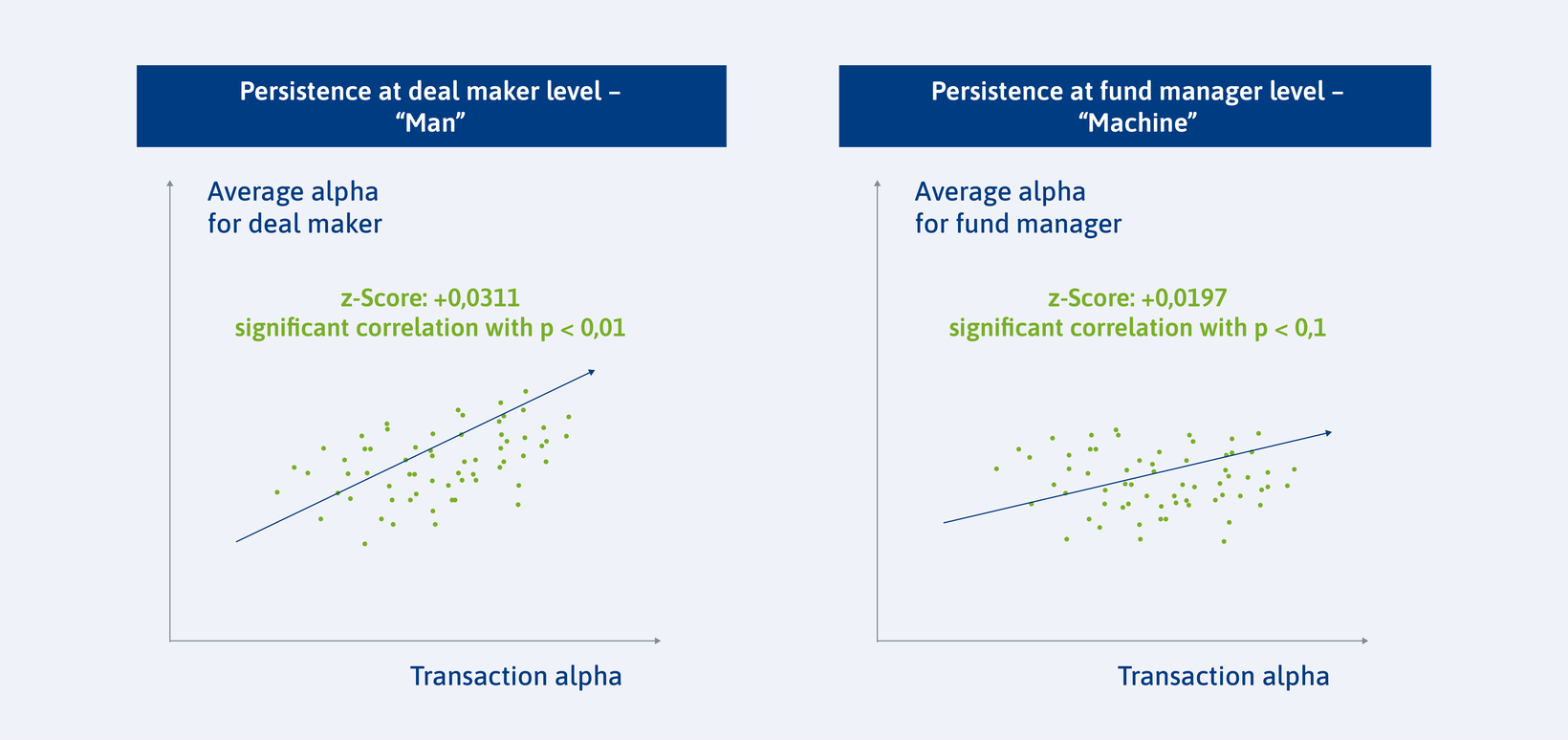

- Prior performance of individuals directly involved in transactions is a stronger indicator than fund level performance

- Private equity delivers an average alpha of 9.9 per cent above comparable stock market returns

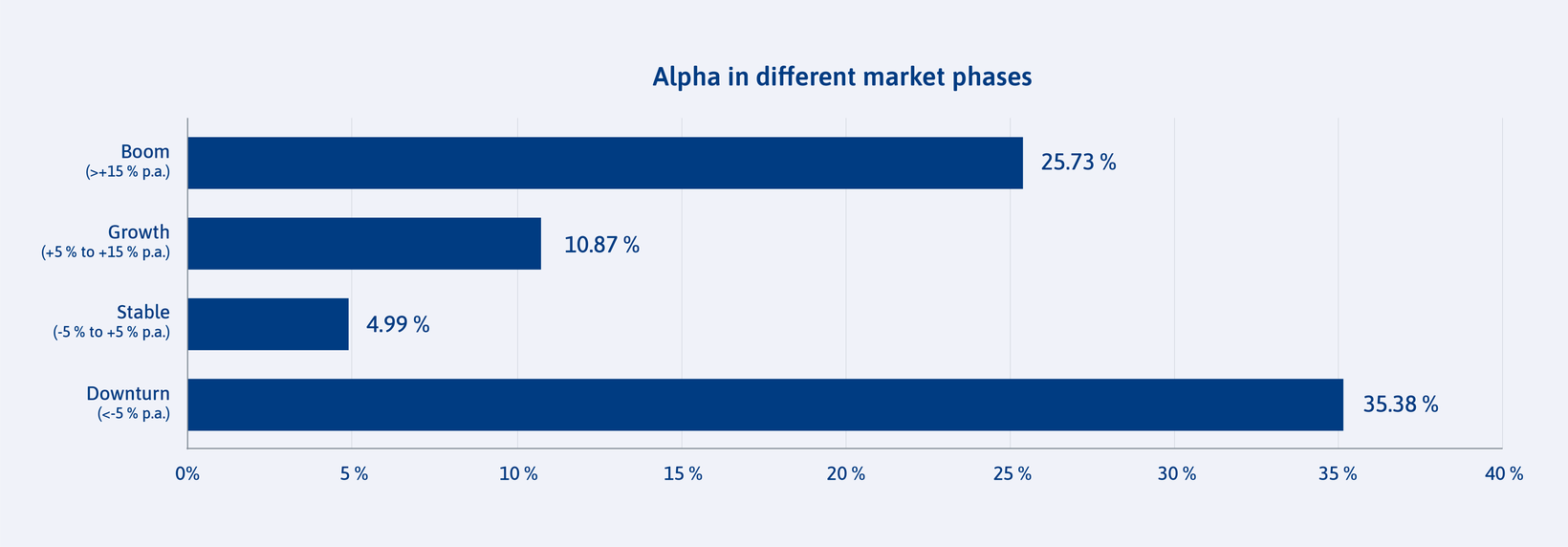

- In periods of crisis, private equity even achieved 35 per cent alpha compared with stock market returns

- Study carried out in collaboration with Professor Gottschalg, (HEC

Paris) based on 4,300 private equity transaction

Golding Capital Partners, one of Europe's leading independent asset managers for alternative investments, has analysed the magnitude and repeatability of alpha returns from private equity investments compared with the stock market. The study carried out in association with Professor Oliver Gottschalg from HEC School of Management Paris shows that the excess return from private equity is persistent over the period 2000-2021. The average alpha compared with similar stock market investments is 9.9 per cent, rising to as much as 35 per cent during periods of crisis. The study indicates that the driver for recurrence of attractive alpha is not the track record at the asset manager level, but rather the earlier performance of the individuals directly involved in the respective transactions.

The current study is the fifth time that Golding has worked with Professor

Gottschalg to analyse the excess return from private equity compared with the

public markets, by calculating the alpha factor delivered by in private equity

transactions. The latest survey took a particularly close look at human

expertise involved.

“There has been a lively ‘man vs. machine’ debate for years now. What is more

important: the track record of the individuals who were responsible for a given

transaction, or the track record of the fund manager at the corporate level? Our study

shows clearly that, with private equity investments, individual human expertise is the

driver, in contrast to the stock markets. For investors, this means it is not a good

idea to rely automatically on the size or reputation of a given fund manager. “When

selecting fund managers, they rather have to understand how the team is put together and

what the individuals involved have contributed in the past”, explains Jakob Schramm,

Partner at Golding Capital Partners.

Jeremy Golding, Founder and Managing Partner of Golding Capital Partners, adds: “Experienced asset managers with a good network can really add value here. We don’t invest in a brand name, but rather follow the people with a sustained track record of success. And for that, our strong personal relationships, based on trust and often going back many years, are worth their weight in gold. Once again the numbers are unequivocal – private equity offers enormous return potential.”

Significant alpha across all market phases and segments – especially at times

of crisis

In the breakdown of alpha for individual market phases, we

distinguish between boom times, relatively stable market phases and periods of

retrenchment in the stock markets. During recessionary times with poor stock market

performance, alpha for private equity is particularly high, at an average of 35 per cent

over the comparable return from public markets. In phases of rapid economic growth with

stock markets appreciating by over 15 per cent p.a., alpha comes to some 26 per cent, by

contrast. In an environment of moderate growth, private equity also generates an alpha

of nearly 11 per cent. In a stable environment with a slightly positive or slightly

negative stock market return, alpha is still 5 per cent.

In terms of the individual market segments, alpha is also significant across

the most diverse sectors of the economy. The excess return is particularly

marked in the communications and energy sectors, at 15.5 per cent and 13.6 per

cent, respectively. Alpha was less strong in the consumer goods and healthcare

sectors, with figures of 8.1 per cent and 8.5 per cent, respectively.

The respective metrics were adjusted in order to enable a direct comparison between the returns from listed shares and private equity. Three effects were factored in for listed shares: i) the timing of cash inflows and outflows, ii) the effect of sector performance on the individual company and iii) the leverage effect, i.e. the gearing of a private equity investment compared with a publicly quoted company. The return from private equity transactions was also adjusted. The discount rate for reinvesting cash flows was a stock market index and not the internal rate of return, as with the standard IRR. The difference between the two returns is the alpha of private equity.

Long-term, broad-based dataset provides evidence of recurrent excess

return over listed shares

The alpha study is based on data from

around 4,300 individual realised transactions in the Golding transaction

database. This dataset not only makes it possible to calculate average figures

for alpha, but also to differentiate between individual market phases and

segments. Furthermore, the study goes beyond the scope of earlier investigations

by not only examining absolute return metrics such as IRR or TVPI, but also the

alpha outperformance.

The results provide strong empirical evidence for

the positive persistence of private equity’s alpha factor over a longer

timeframe.

“Investors cannot rely on absolute return measures as an indicator of the future performance of private equity funds. Alpha, however, is eminently suitable as a metric for selecting fund managers. Funds that achieved above-average alpha in the past have a higher probability than other funds of generating above-average alpha in the future”, explains Professor Oliver Gottschalg from HEC School of Management.

Details of the study can be downloaded here: Study on the

Alpha of Private Equity Investments